After the recent historic increases in home prices, it seems that every housing expert is debating whether the market is about to crash. There is evidence that price growth has started to slow down, however, most experts still predict positive price growth for 2022. If you are a consumer and are thinking about buying a home, this is relevant to you: Should you wait for prices to come down before buying? Or should you jump into the market before prices continue to climb? In this blog post, we attempt to look at the key housing demand and supply drivers to better understand the market situation and its risks.

At Mirabilis Homes, we do not believe that the housing market is about to implode. Our base-case scenario calls for a significant slowdown in prices. We believe that price growth will flatten and can even turn slightly negative in the next 18-24 months. Although significant risks exist, we believe that a market crash (double-digit price decline) is a low probability scenario.

Just as in any other free market, the housing market is all about demand and supply. These two forces directly dictate home prices. There are many other variables that can directly or indirectly affect demand and supply but at the end of the day, it is these two variables that cause prices to go up or down. In recent years demand has been significantly outpacing supply. This demand/supply imbalance resulted in record price growth of 18.8% and 10.4% in 2021 and 2020 respectively (S&P CoreLogic Case Shiller).

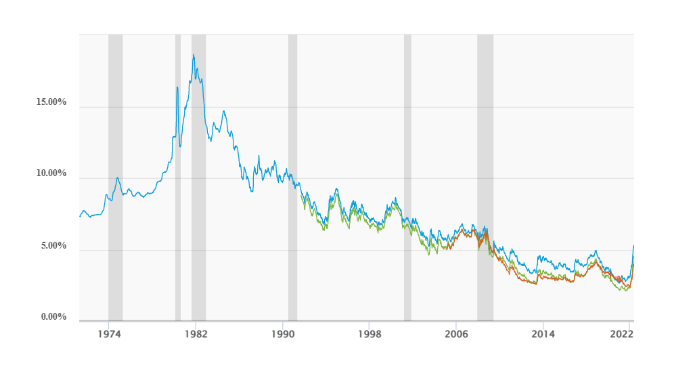

One of the key reasons why demand has been strong is the low-interest-rate environment. When interest rates fall, mortgage rates follow, and housing affordability increases, which causes more people to want to buy a home. With lower rates, monthly payments decrease and thus people can afford more, so more people enter the market causing an increase in demand for homes. Right now, there is a record number of renters – about 44 million households vs 30 million just 20 years ago – sitting on the sidelines. About 80% of these renters want to become homeowners, according to a Freddie Mac survey. So, when conditions become favorable these renters might jump into the market, driving prices up.

Another reason why demand has been strong is the new Wall Street money pouring into the single-family rental (SFR) sector in recent years. Giant firms such as Blackstone, Amherst, and many other Wall Street firms backed by banks are amassing huge rental portfolios. In the short term, they are generating additional demand and driving prices higher. However, the longer-term implications are more serious. Their purchases are reducing the inventory of for-sale properties and permanently reducing the supply of homes which in turn drives prices higher since there is less inventory available for home buyers. While investors today purchase only about 20% of homes, they are growing rapidly and represent a consistent source of demand in the market. If this trend were to continue, many American families will likely be priced out of the market and will be forced to rent precisely from the firms that denied them their homeownership dreams.

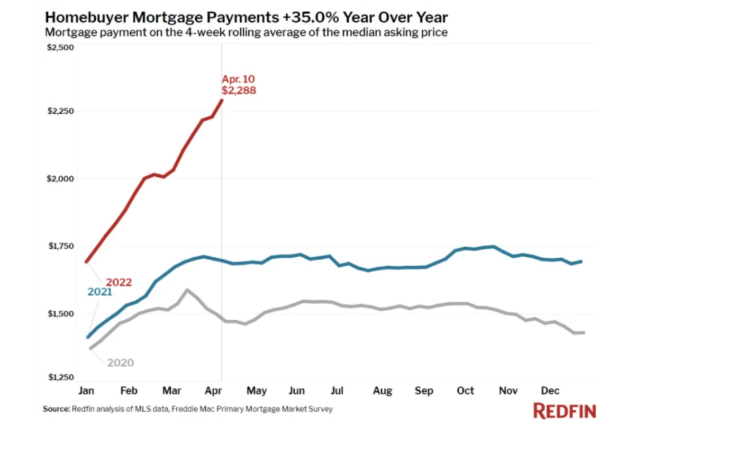

Today demand is clearly slowing down. Price reductions in listed homes continue to increase. In the week ending May 13th, price decreases accelerated to their fastest pace since at least 2015 while price increases were minimum. Additionally, this year mortgage rates have increased at a record pace and there are early signs that demand has moderated as a result. The higher rates have significantly increased monthly payments for Americans to $2,288 on a median-priced home according to Redfin (see below). As a result, the NAR estimates that 15% of first-time homebuyers will be priced out of the market this year. Mortgage applications for home purchases in the last week of April were down 11% from a year ago. Furthermore, Redfin’s Homebuyer Demand Index – a measure of requests for home tours declined 3% in April. However, for the market to crash we would need to see a considerable decrease in demand coupled with increasing supply. Demand is slowing down but not in a drastic way and is slowing down from record highs so homebuyer demand is still healthy.

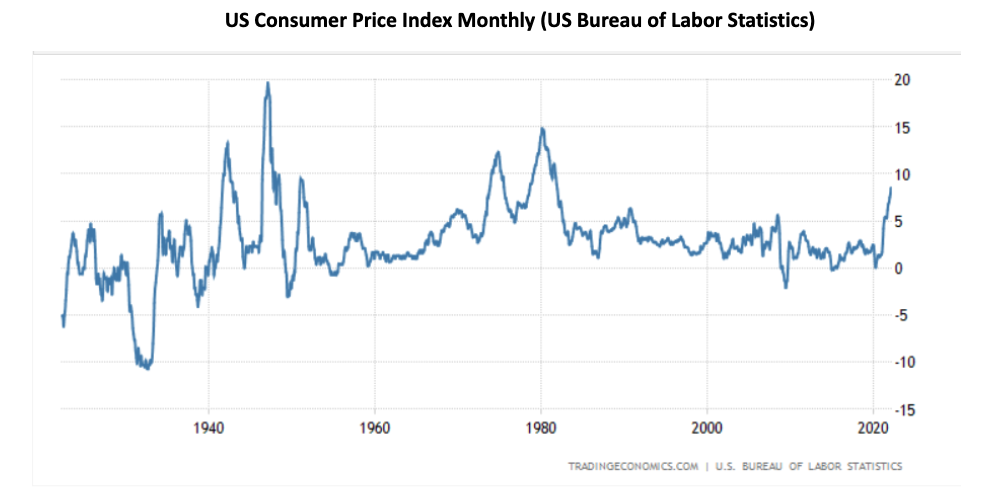

Inflationary pressures have started to appear in the economy. The pandemic and recent Russia- Ukraine conflict have severely disrupted the global supply chain, increasing the cost of energy, food, and many other consumer products as a result. Inflation in the US has reached a 40-year high. These inflationary forces will further reduce demand for homes. As inflation increases, consumers spend a larger share of their income on basic necessities such as food and transportation and have less discretionary income to spend/save for a new home. Inflation also has a negative effect on consumer sentiment which can further depress demand. Let’s now take a look at the other side of the equation: supply.

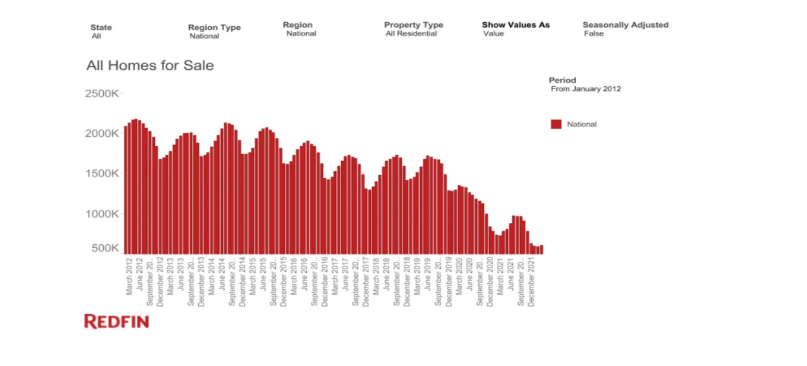

Supply, measured as inventory, is at record lows. Until inventory recovers to more normalized levels it is very unlikely that the market will crash. The below chart from Redfin gives us a good idea of how inventory today compares to the last ten years. In the 2012-2017 period, inventory stood at about 2M during the peak summer months. Today, homes available for sale stand at slightly more than 0.5M or almost a 75% reduction.

The low number of available homes for sale is what has prompted the recent bidding wars. While demand might be decreasing, the extremely low number of available homes for sale will continue to put upward price pressure on the housing market. The way for home prices to come down is when sellers are unable to sell their homes. Only when homes sit on the market for extended periods of time will sellers begin considering lowering their prices so days on market (DOM) becomes a significant metric. Days on market have seen a similar trend as inventory since 2012, however pre-pandemic, it took on average about 45 days to sell a home. Today it takes about 17 days.

Given the low levels of inventory, one must ask the question: Is there anything that is likely to cause a sudden spike in inventory levels?

Given the low levels of inventory, one must ask the question: Is there anything that is likely to cause a sudden spike in inventory levels?

The first relevant measure is new listings. This metric is trending downwards. It seems people do not want to sell into a softening market. More than half of homeowners have a mortgage rate below 4% so unless they get top money for their property, they are unlikely to sell in the current environment. Additionally, Americans are sitting on a record amount of home equity, over $10 trillion. The average mortgage holder now has $185,000 of home equity so if Americans need cash, they can always monetize their equity instead of selling their property.

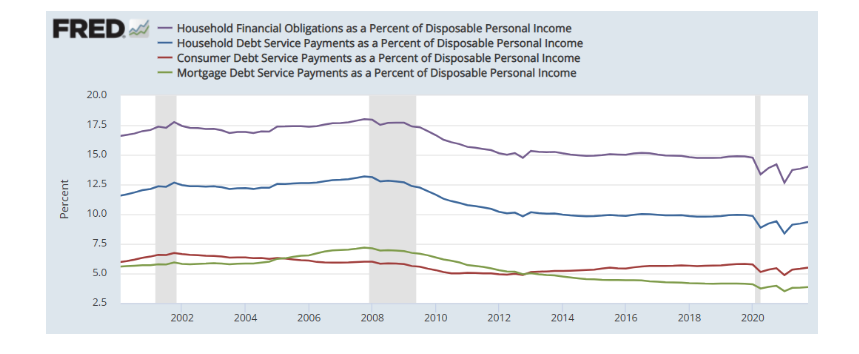

Another way for inventory to increase would be foreclosures. There are multiple indications that we won’t have a foreclosure crisis any time soon. Mortgage delinquencies have dropped for almost two straight years. Mortgage debt service payments (as % of disposable income) are near a multidecade low at 3.8% (versus 7% in 2007). Overall Household Financial Obligations are also close to a two-decade low.

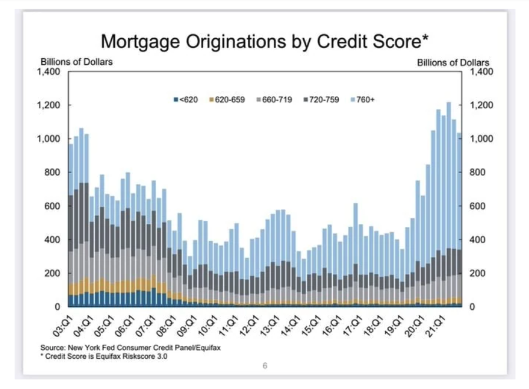

Additionally, the average credit score on mortgage originations has been very strong. Oh, and we already mentioned that Americans are sitting on record levels of home equity, a total of more than $10 trillion in the US.

The last way for inventory to increase would be through new construction. We won’t elaborate much on this topic as it usually takes many years for new construction to be reflected on inventory. However, residential construction (permits and starts) has not seen a significant increase from its depressed levels so we do not expect new construction will significantly impact inventories in the following years. The lack of construction seen in the previous decade will have effects for the following decade. There is a substantial deficit in new home inventory. Experts estimate this gap is between 1.5 and 5 million units.

While demand has been softening, the current low levels of inventory are likely to keep the demand/supply equation in or close to balanced. Our expectation is that price growth will significantly soften and might even turn negative in the next 18-24 months but we believe it is highly unlikely that we will experience a market crash. However, things can quickly change and there are many uncertainties in the world today (pandemics, geopolitical confrontations, inflation, etc.) so it is important to keep an eye on the data and revisit key metrics periodically.