Purchasing a home is an exciting milestone in a person’s life, and it often requires careful financial planning and preparation. One aspect that plays a significant role in the home-buying process is your credit score. Your credit score not only determines whether you qualify for a mortgage or home-buying program but also affects the interest rates and terms you receive. Even if you decide not to buy, your credit history might affect your probability of renting your dream place. In this article, we will explore the topic of credit scores and their impact on buying a home. Additionally, we will provide practical tips on how to improve your credit score and increase your chances of securing your dream home.

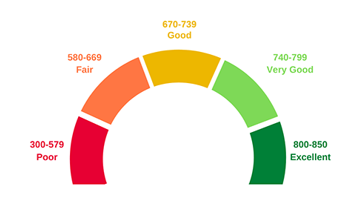

Credit Score Scale

Understanding Credit Scores: To embark on the homeownership journey, it’s essential to comprehend what credit scores are and how they are calculated. Credit scores are three-digit numbers that represent your creditworthiness and financial health. Lenders utilize these scores to assess the level of risk involved in extending you a loan. The most commonly used credit score model is the FICO score, which ranges from 300 to 850. The higher your credit score, the better your chances of securing favorable mortgage terms.

Minimum Credit Score Requirements: While there isn’t a universal credit score requirement to buy a home, most lenders have specific thresholds. Generally, a credit score of 620 or above is considered the minimum requirement for conventional mortgage loans. However, government-backed loans, such as FHA loans, may accept credit scores as low as 500, albeit with certain conditions. It’s important to note that having a higher credit score opens doors to better loan options and lower interest rates.

Factors Influencing Your Credit Score: Several factors contribute to your credit score and understanding them can help you make informed decisions. The primary elements include:

Steps to Improve Your Credit Score: If your credit score is below the desired range for buying a home, don’t worry! There are several effective strategies to improve your creditworthiness:

Patience and Persistence: Improving your credit score is a gradual process that requires patience and persistence. It may take time to see substantial improvements, but every positive step you take will contribute to your overall financial health. Keep your eye on the goal of homeownership and stay committed to responsible financial habits.

Your credit score plays a vital role in the home-buying process, impacting your eligibility for a mortgage and the terms you receive. By understanding credit scores and implementing strategies to improve them, you can increase your chances of securing your dream home. Remember, building a strong credit profile takes time and effort, but the rewards are well worth it. Take control of your financial future and embark on the path toward homeownership with confidence.

At Mirabilis Homes, we not only aim to help our clients achieve homeownership with a 1% down payment but also assist them in building their credit along the way. We understand the importance of a good credit score when it comes to securing a mortgage or other financial opportunities. When you apply to our INTRO Program, we only run a “soft check”, which means your application won’t impact your credit score. Additionally, we have partnered with Esusu to report our client’s on-time rent payments to the leading credit agencies. By consistently making these payments on time, clients can establish a positive payment history, which can have a significant impact on their credit score. We are committed to supporting our clients throughout their homeownership journey, including helping them improve their creditworthiness along the way.

At Mirabilis Homes, we are dedicated to not only making homeownership accessible but also helping our clients strengthen their financial standing through strategic partnerships like the one with Esusu.

All Rights Reserved © Mirabilis Homes 2022

All Rights Reserved © Mirabilis Homes 2023